Tax Benefits of Offering Health Insurance to Foreign Workers in Canada (2026 Guide for Employers)

If you hire temporary foreign workers through Canada’s Temporary Foreign Worker Program, you’re generally required to provide and pay for private health coverage during any period they aren’t protected by a provincial or territorial health plan.

But we’ve noticed something that most employers don’t fully consider: when done correctly, that same coverage could significantly reduce your business’s taxable income.

Canadian employers are under real pressure. Labour costs are up, and health plan costs are rising. Plus, the administrative burden of TFWP compliance isn’t getting lighter.

The tax efficiency built into properly structured employer health coverage is one of the most underused financial tools for businesses that hire foreign workers. Here’s what you need to know.

How is Employer-Paid Health Insurance Taxed in Canada?

Employer-paid premiums for group health and dental plans are typically deductible business expenses in Canada.

The CRA treats them similarly to other forms of employee compensation: they reduce your taxable business income, dollar for dollar.

What makes health benefits especially powerful is the employee side of this equation. In most provinces, employer-paid health and dental premiums aren’t added to the employee’s taxable income, so workers receive coverage tax-free and typically won’t see it reported on their T4.

There are two notable exceptions to this:

Quebec adds employer health premiums to employees’ taxable income for provincial purposes

Certain employer health levies in British Columbia apply separately

CRA guidance on “premiums and contributions to insurance plans” confirms this for qualifying plans.

The result is a double advantage: a deductible for the business and tax-free for most employees.

PHSPs, HSAs, and Group Plans

Not every health spending arrangement qualifies for the most favourable tax treatment. When looking at options for Canadian employers in 2026, here’s what to know:

Private Health Services Plans (PHSPs)

A PHSP is a plan where all (or substantially all) of the coverage is for eligible medical and dental expenses under the Income Tax Act.

When a plan qualifies as a PHSP, incorporated employers can generally deduct 100% of premiums paid on behalf of employees — including temporary foreign workers.

Here’s the key test: the plan must be genuine insurance for health expenses, not a general reimbursement account in disguise.

Group Health Plans

Traditional employer-sponsored group health, dental, vision, and paramedical plans are usually structured to meet CRA’s PHSP requirements.

Premiums paid to an insurance carrier on behalf of employees are generally deductible to the business and non-taxable to employees in most provinces.

These are the most common structures among mid-sized and larger employers.

Health Spending Accounts (HSAs)

HSAs structured as PHSPs allow incorporated employers to reimburse eligible health expenses on a fully deductible basis. Employees receive reimbursements tax-free.

This approach offers flexibility for workforces with varied health needs and cost predictability since employers set contribution limits in advance.

Owner-Operators and Unincorporated Businesses

Section 20.01 of the Income Tax Act caps PHSP deductions for sole proprietors and self-employed individuals on their own coverage.

However, premiums paid for arm’s-length employees — including foreign workers under your LMIA — remain generally deductible as a business expense.

Even small agricultural operations hiring a handful of TFWs can access meaningful write-offs.

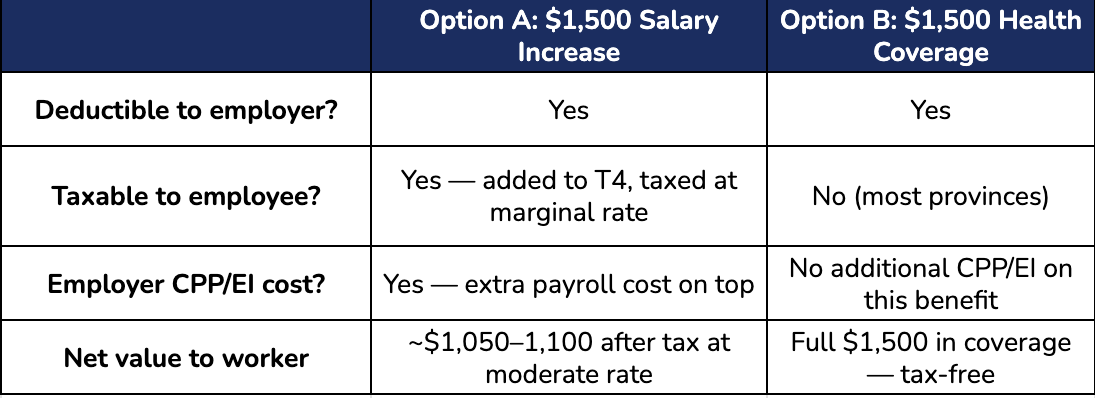

Doing the Tax Math

The instinct when investing in workforce compensation is to raise wages. But from a tax efficiency standpoint, employer-paid health benefits deliver more value per dollar for both sides.

Consider a simple comparison. You want to invest an additional $1,500 in compensating a foreign worker:

For foreign workers who often have no access to family or spousal coverage and face real health risks during physically demanding contract periods, comprehensive benefits represent genuinely high-value compensation.

This gives employers a powerful tool: meaningful improvement to total compensation without ratcheting wages upward, at a lower total cost to the business.

You can recruit and retain quality workers more effectively while spending less than you might expect.

Specific Tax Advantages When You Insure Foreign Workers

For TFWP employers, properly structured health coverage offers advantages that go beyond the general tax benefits described above.

Compliance and Deductibility Align

Under TFWP regulations, employers must provide and pay for private health coverage during any period a worker is not covered by a provincial plan.

Coverage purchased to satisfy this obligation — such as a TFW-specific plan that includes emergency medical, supplementary health, and income replacement — can generally be treated as a deductible expense if it meets PHSP or group plan criteria.

In many TFWP scenarios, you’re spending money you’re legally required to spend anyway; structuring it correctly ensures CRA treats it as favourably as possible (without risking mistakes).

No Taxable Benefit Created for Most Workers

Where a plan qualifies, and the province treats employer health premiums as non-taxable, temporary foreign workers are generally taxed the same way as other employees.

Their coverage costs them nothing out of pocket and nothing at tax time — a meaningful benefit for workers who often send significant portions of their income home to their families.

Supports ESG, Recruitment, and Retention

Employers face growing pressure to demonstrate responsible labour practices, including genuine care for non-resident workers.

Offering structured, documented health coverage positions your business as a preferred employer — without creating additional taxable income for the people you’re trying to support.

The key throughout is proper documentation and administration. Benefits that are genuinely part of a qualifying plan are treated favourably by CRA. Ad hoc or poorly structured arrangements can lose that protection entirely.

Putting It Into Practice with The FWCHP

The money you spend on foreign worker coverage can reduce your taxable income and deliver greater real value to workers than an equivalent wage increase.

Plus, you’ll position your business as the kind of employer quality workers choose to return to season after season.

Want to understand how the FWCHP fits into your benefits and tax planning for 2026?

Contact us today to speak with one of our advisors about structuring foreign worker health coverage that works for your business — compliantly and cost-effectively.

This article provides general information about taxes and health coverage for temporary foreign workers. It is not legal advice; always consult your immigration and legal advisors about your specific situation.

Looking to provide your foreign workers with the necessary healthcare coverage?

Click through the video below to learn about the FWCHP.